Most mystery shoppers don’t think about quarterly taxes until April — and by then, they’re already behind. The IRS expects you to pay taxes as you earn money, not just at year end. Miss those payments and you’ll owe penalties on top of your bill, even if you pay everything off in full when you file. This guide breaks down exactly how quarterly estimated taxes work for mystery shoppers, how to calculate what you owe, and how to pay without the stress.

Important: We’re mystery shoppers, not tax professionals. This article is for general information only. Tax rules change, and everyone’s situation is different. Please find a trusted tax professional in your area before making decisions about your estimated tax payments. Getting this right is worth the cost of professional advice.

Why Mystery Shoppers Have to Pay Quarterly

When you work a regular job, your employer withholds taxes from every paycheck. You never see that money — it goes straight to the IRS. Mystery shopping doesn’t work that way. The companies that hire you pay your full fee with no withholding. That means you’re responsible for sending taxes to the IRS yourself, on a schedule the IRS sets.

The US tax system is pay-as-you-go. You owe taxes throughout the year as you earn income, not just when you file your return in April. Quarterly estimated taxes are how self-employed people and independent contractors meet that requirement.

If you expect to owe at least $1,000 in federal taxes for the year — after accounting for any withholding from a regular job and any credits — the IRS generally requires you to make quarterly payments. Most active mystery shoppers hit that threshold. At $20 per shop and 50 shops a year, you’re earning $1,000 in mystery shopping income alone, and your tax bill on that could easily top the $1,000 trigger.

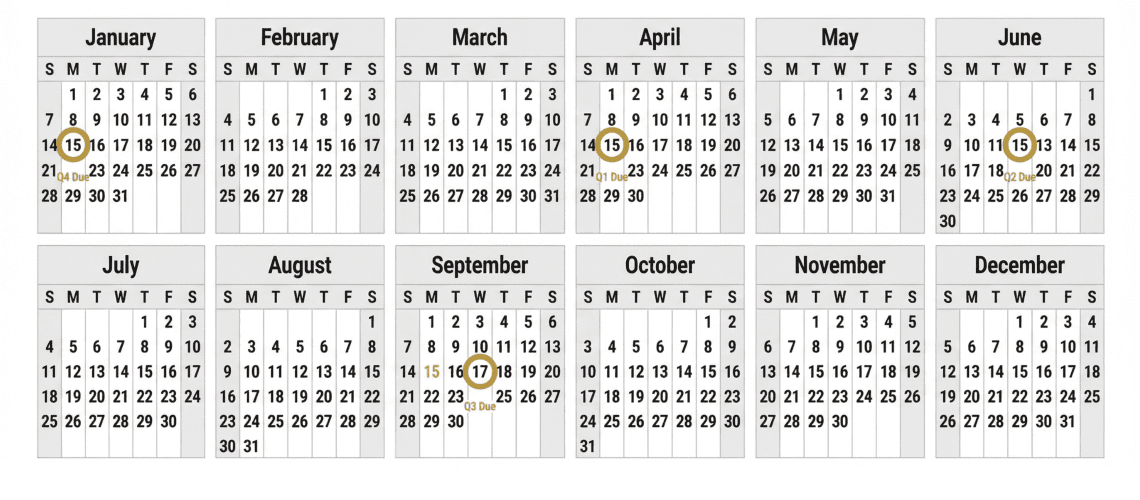

The 2026 Quarterly Tax Due Dates

These are the four deadlines for your 2026 estimated tax payments. Mark all of them in your calendar now.

Q1 Payment (Jan–Mar income): April 15, 2026

Q2 Payment (Apr–May income): June 15, 2026

Q3 Payment (Jun–Aug income): September 15, 2026

Q4 Payment (Sep–Dec income): January 15, 2027

A couple of things worth knowing about those dates. First, the “quarters” don’t split the year evenly. Q1 covers three months, Q2 covers two, Q3 covers three, and Q4 covers four. That’s just how the IRS does it. Second, if a due date falls on a weekend or federal holiday, it shifts to the next business day — but plan for the listed date and you’ll never be caught off guard.

There’s also one useful shortcut: if you file your full 2026 tax return and pay everything you owe by January 31, 2027, you can skip the Q4 payment due January 15. Most mystery shoppers find it easier to just make the Q4 payment on time and file their return in February or March without the rush.

How to Figure Out What You Owe Each Quarter

You have two methods for calculating your quarterly estimated tax payments. Both are IRS-approved. Pick the one that fits how your income flows throughout the year.

Method 1: Safe Harbor

The safe harbor method protects you from underpayment penalties even if you end up owing more than you paid in. It’s the simplest approach and works well for most mystery shoppers.

Here’s how it works: Pay at least 100% of last year’s total tax bill across your four quarterly payments. Divide what you paid last year by four and send that amount each quarter. As long as you hit that number, the IRS won’t charge you a penalty — even if your actual tax bill ends up higher when you file.

If your prior-year adjusted gross income was over $150,000 (or $75,000 if married filing separately), the threshold bumps up to 110% of last year’s tax. That’s a higher bar, but the same logic applies.

Example: Your total federal tax bill for 2025 was $4,200. Using safe harbor, you’d pay $1,050 per quarter in 2026 ($4,200 ÷ 4). Even if your mystery shopping income grows and your actual 2026 bill ends up being $5,500, you won’t owe an underpayment penalty — because you paid 100% of last year’s tax on time.

Safe harbor is especially useful if your mystery shopping income is hard to predict. You know last year’s number exactly, so there’s no guesswork involved.

Method 2: Estimate Your Actual 2026 Tax

The second method is to estimate what you’ll actually owe for 2026 and pay 90% of that across your quarterly payments. This works better if your income is consistent and predictable, or if your mystery shopping income is significantly higher or lower than last year.

To use this method, you estimate your total income for the year, subtract your deductions (including mileage, business expenses, and half of your self-employment tax), apply the current tax brackets, and add self-employment tax on top. Then divide that projected total by four.

The math takes more effort, but it can mean lower quarterly payments if you’re earning less than last year. Our Mystery Shopping Tax Guide covers the self-employment tax calculation in detail, and the Quarterly Tax Estimator calculator can help you run the numbers for your situation.

What Taxes You’re Actually Paying

As a mystery shopper, your quarterly payments need to cover two separate taxes — not just one. A lot of new shoppers miss this and end up short.

Self-Employment Tax

Self-employment tax covers Social Security and Medicare. When you work a regular job, you pay 7.65% and your employer pays the other 7.65%. As an independent contractor, you pay both sides — 15.3% total. That’s on top of income tax, not instead of it.

The good news: you can deduct half of your self-employment tax from your gross income when calculating your income tax. It doesn’t eliminate the cost, but it softens the hit.

Self-employment tax only kicks in on net earnings of $400 or more per year from self-employment. If mystery shopping is a very occasional side activity and you earn less than $400 net after deductions, you won’t owe SE tax. Most consistent mystery shoppers exceed that threshold easily.

Federal Income Tax

Income tax is based on your total taxable income from all sources — mystery shopping earnings, wages from a regular job, investment income, and anything else. Mystery shopping income is added to everything else and taxed at your marginal rate.

Your quarterly payments need to cover both self-employment tax and your share of income tax on mystery shopping earnings. Forgetting one of them is the most common reason mystery shoppers find themselves with a surprise tax bill in April.

How to Actually Make the Payments

The IRS makes payment straightforward. You have a few good options.

| Payment Method | Cost | Best For |

|---|---|---|

| IRS Direct Pay | Free | One-time payments from your bank account — fast and simple |

| EFTPS (Electronic Federal Tax Payment System) | Free | Scheduling payments in advance; requires one-time enrollment |

| IRS2Go app | Free | Mobile payments when you’re on the go |

| Debit or credit card | Processing fee (~1.82–1.99%) | Convenience if you need rewards points or have cash flow timing issues |

| Check or money order | Postage | Still works, but allow 7–10 days for processing |

IRS Direct Pay is the easiest choice for most mystery shoppers. Go to IRS Direct Pay, enter your payment amount, select “Estimated Tax” as the reason, and confirm. You’ll get an immediate confirmation number — save it.

If you want to set payments on autopilot, enroll in EFTPS and schedule all four payments at the start of the year. You only need to know last year’s tax bill to do this using the safe harbor method. Then you don’t have to think about it again until you file.

Don’t pay by check at the last minute. Paper checks can take 7–10 business days to process. If you mail a check on the due date, the IRS may mark it late. Use Direct Pay or EFTPS for any same-week payments and you’ll get confirmation immediately.

What Happens If You Miss a Payment

Missing a quarterly estimated tax payment isn’t a criminal offense — but it does cost you money. The IRS charges an underpayment penalty calculated from the due date of the missed payment to the date you finally pay. The current rate is around 8% annually, compounded daily.

For a $500 missed quarterly payment, that’s roughly $10 in penalties per month. It’s not devastating, but it adds up over multiple quarters. And the penalty applies even if you pay your full balance when you file in April. Paying late in April doesn’t erase the penalty for missing the September or January deadline.

If you miss a payment, pay it as soon as you can. Every day you wait adds to the penalty. Don’t wait until the next quarter’s due date — make the payment now and cut the damage short.

When You Might Avoid the Penalty

The IRS can waive the underpayment penalty in certain situations. These include unusual circumstances like a natural disaster, a serious illness, or a first-time penalty if you have a good compliance history. They won’t waive it just because you forgot or didn’t know. The safe harbor method is the cleaner way to avoid the penalty altogether — use it if your income is unpredictable.

Mystery Shopping and a Day Job: How It Interacts

Many mystery shoppers also have a regular W-2 job. If that’s you, there’s a smarter alternative to making quarterly payments: adjust your W-4 withholding at your day job to cover the extra taxes from mystery shopping.

Ask your employer’s HR department for a new W-4 form. On it, you can specify an additional flat dollar amount to withhold from each paycheck. If your mystery shopping income is likely to add $2,000 to your annual tax bill, you’d add roughly $77 in extra withholding per biweekly paycheck ($2,000 ÷ 26). That handles your mystery shopping taxes automatically through your regular paycheck — no quarterly payments needed.

This works best when your mystery shopping income is fairly consistent. If your shop volume spikes and drops throughout the year, quarterly payments may be more accurate.

Which approach is right for you? If you have a day job and stable mystery shopping income, adjusting your W-4 is often the easier path. If mystery shopping is your only income, or if your shop volume varies a lot, quarterly payments give you more control. A tax professional can help you decide based on your full picture.

A Simple System for Staying on Top of Quarterly Taxes

The mystery shoppers who handle this well don’t wing it at deadline time. They build a simple system at the start of each year and stick to it. Here’s one that works.

Step 1: Open a Dedicated Tax Savings Account

Set up a separate savings account just for taxes. Every time you get paid for a shop, transfer a percentage to that account before you spend anything. Most mystery shoppers set aside 25–30% of gross mystery shopping income. That covers self-employment tax and income tax for most tax situations.

This doesn’t have to be exact. The goal is to have money set aside when a payment comes due — not to scramble every quarter.

Step 2: Log Income Every Month

Keep a simple record of what you earn from mystery shopping each month. A spreadsheet works fine. At the end of each quarter, you’ll know exactly how much you made and can check whether your estimated payment covers it.

Step 3: Pay on the Due Date, Not Before or After

There’s no benefit to paying early. The IRS doesn’t give you credit for front-loading payments. Pay on or just before each due date and let your tax savings account earn interest in the meantime.

Step 4: Adjust as You Go

If your mystery shopping income jumps significantly in Q3, increase your Q3 or Q4 payment to match. If it drops, you can pay less — as long as you’re still on track to hit 90% of your actual liability or 100% of last year’s tax via safe harbor. Check in at the end of each quarter and adjust if needed.

Quarterly Taxes Are Manageable — Just Don’t Ignore Them

Quarterly estimated taxes feel overwhelming when you first hear about them. Once you set up a system, they become a routine part of mystery shopping. Four payments a year, 10 minutes each to submit online, done.

The shoppers who get into trouble are the ones who ignore quarterly taxes all year and then face a large bill plus penalties in April. Don’t be that person. Set the four due dates in your calendar today, put aside a percentage of every shop payment, and pay on time.

For the full picture on mystery shopping taxes — including self-employment tax rates, Schedule C deductions, and what records to keep — check out the Mystery Shopping Tax Guide. And use the Quarterly Tax Estimator to get a quick estimate of what you might owe this year.

More back-office resources for mystery shoppers:

📋 Mystery Shopping Tax Guide — self-employment tax, Schedule C, deductions explained

🧮 Quarterly Tax Estimator Calculator — estimate your payments in minutes

🚗 Mileage Tracking Guide — capture your biggest tax deduction

💰 How Much Do Mystery Shoppers Make? — realistic income expectations